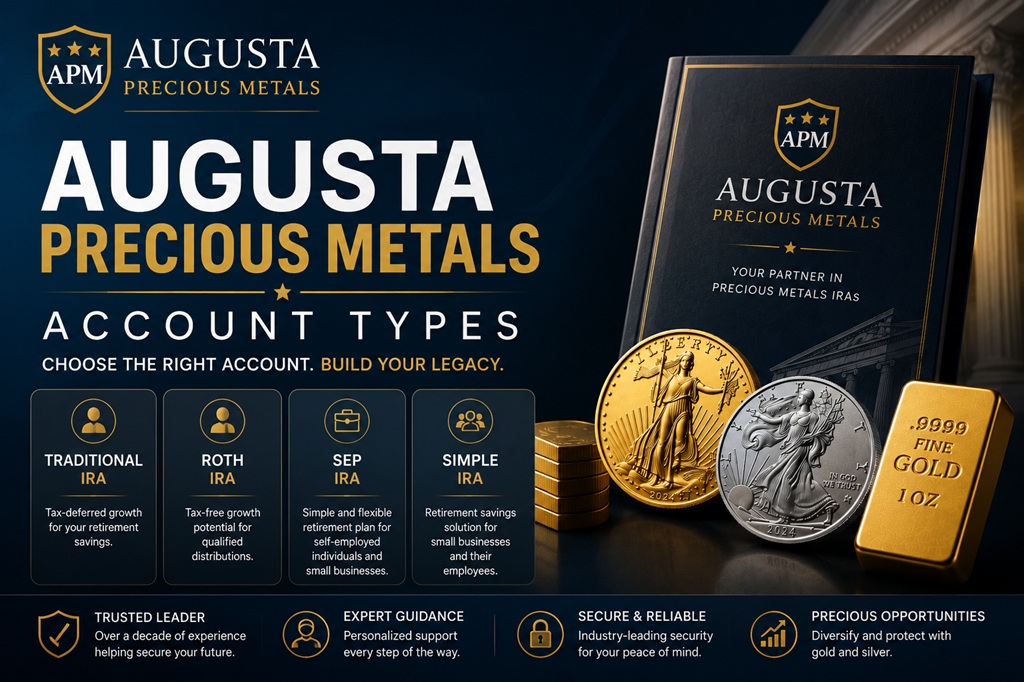

Augusta Precious Metals Account Types Explained

TL;DR: An Augusta precious metals account can be structured as a Traditional, Roth, SEP, or SIMPLE IRA, plus a spousal arrangement, each the same federal wrapper holding IRS-eligible gold and silver instead of paper. The structural choice between them is set by IRS rules, not by Augusta, and the practical entry gate is a $50,000 minimum to open. This guide explains each type structurally and who it suits.

Disclosure: This site has a partnership relationship with Augusta Precious Metals and may earn a commission from accounts opened through the contact methods on this site, in line with [Federal Trade Commission](https://www.ftc.gov/) affiliate-disclosure rules under 16 CFR Part 255. Editorial coverage reflects Augusta's published positioning and the current IRS rules governing self-directed precious-metals IRAs.

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Augusta Precious Metals Reviews is not a licensed financial advisor, CPA, or attorney. Consult a qualified professional before making investment or tax decisions.

| Account Type | Structural Snapshot |

| **Traditional IRA** | Pre-tax wrapper, the usual rollover destination for a 401(k) or Traditional IRA |

| **Roth IRA** | After-tax wrapper, funded with already-taxed dollars or by conversion |

| **SEP IRA** | Employer-funded wrapper for the self-employed and small-business owners |

| **SIMPLE IRA** | Small-employer salary-deferral wrapper |

| **Spousal arrangement** | Two separate individual accounts, one fundable on household earned income |

What Account Types Does Augusta Precious Metals Offer?

An Augusta precious metals account can be structured five ways: a Traditional IRA, a Roth IRA, a SEP IRA, a SIMPLE IRA, or a spousal arrangement built from two individual accounts. The metal inside is identical across all of them. What separates one structure from the next is the tax timing and who is allowed to fund it.

Picture the account type as a container and the metal as the contents. The container decides when tax is paid and who can put money in. The contents stay the same IRS-eligible bullion and coins no matter which container you pick. That single distinction is the backbone of this entire page, and it is the part most first-time savers get wrong.

Why does the type matter so much if the metal is the same? Because the choice of structure decides the deduction now, the tax later, and who is even eligible to open it. A 28-year-old freelancer and a 62-year-old rolling over a pension do not belong in the same structure. The wrapper, not the bullion, is where that difference lives.

Two facts hold steady no matter which of the five you pick, so this page sets them aside up front. The first is the entity model. Augusta is the metals dealer, and a separate IRS-approved trustee legally holds the account, an arrangement explained end-to-end on the Augusta gold IRA overview and not restated here. The second is the price of entry. The minimum to open is $50,000 regardless of type, against a category floor of roughly $5,000.

Neither of those changes between a Traditional, a Roth, a SEP, or a SIMPLE. They are constants. Everything that actually varies, the tax timing, the eligibility test, and who the structure is built for, is what the rest of this page works through, one type at a time. Which one belongs to a given saver is the real question, and it has a different answer for a salaried employee than for a freelancer with fluctuating self-employment income.

How Is a Traditional Augusta Gold IRA Structured?

A Traditional Augusta gold IRA is the pre-tax wrapper. It is the structure most rollovers land in, because the source account, usually a 401(k) or a Traditional IRA, already holds pre-tax money. It broadly suits savers who expect a lower tax bracket in retirement than they carry today.

The pre-tax character is the whole structural point. Money that went in untaxed elsewhere stays untaxed when it moves into a Traditional precious-metals wrapper, so nothing about the rollover triggers a tax event by itself. That is why the Traditional structure is the default landing spot for a 401(k) or Traditional IRA balance rather than a deliberate election. The saver is usually not choosing it so much as inheriting it from the source account.

Who fits this structure? A pre-retiree or retiree with a sizeable pre-tax balance to move, who reasonably expects a lower marginal bracket once the paycheck stops. The classic case is someone in peak earning years today who will draw a smaller taxable income in retirement. That is a structural orientation, not a recommendation, and the bracket projection itself is a tax question for a qualified professional.

The pre-tax wrapper carries one structural trade nobody should miss. The deferral is not forgiveness. Every untaxed dollar inside a Traditional structure is taxed on the way out, and the structure forces those withdrawals to begin in the owner's seventies. A Roth does not. That single contrast is the reason the next section exists, and the dollar mechanics behind it, the contribution limits, deduction phase-outs, and distribution timing, are owned in full by the Augusta gold IRA tax benefits guide rather than restated here.

How does Augusta handle this type at onboarding? Exactly the way it handles every other one. The dedicated agent walks the wrapper choice, a separate custodian opens and funds it, and Augusta states that its representatives earn salaries rather than per-transaction commissions. No structure gets a harder sell than another. Whether the Traditional wrapper is the right pick comes down to the funding source and the bracket expectation, which is a professional's call.

Account-type eligibility and the IRS rules behind self-directed precious-metals IRAs change with new legislation, and the figures here reflect the publication date. A tax professional or IRS-approved custodian should confirm the current treatment for your situation before you act.

How Is a Roth Augusta Gold IRA Structured?

A Roth Augusta gold IRA is the after-tax wrapper. It is funded with dollars that have already been taxed, or through a conversion from a Traditional balance. It broadly suits savers who expect a higher tax bracket in retirement, or who want to leave the position to heirs.

One reversal defines this structure against the Traditional one: the tax is paid going in, not coming out. Pick a Roth wrapper and the bullion grows with no further federal tax bill waiting at the other end, assuming the qualifying conditions are met. The plumbing around the metal does not change at all. Only the moment the tax lands moves.

One property of this container shapes who it suits more than any other. It carries no forced withdrawals during the original owner's lifetime. A Traditional structure makes the owner start drawing money out in their seventies whether they need it or not. This one does not. The position can sit and compound for the owner's whole life, which is the structural reason it appeals to savers focused on what they leave behind rather than what they spend.

There are two ways into this wrapper: fund it directly with post-tax money, or move an existing pre-tax balance into it through a conversion, including a balance already holding physical metal. A conversion swaps the container without touching the coins. The cost and qualifying detail that come with either route are pure tax mechanics, owned end-to-end by the Augusta gold IRA tax benefits page. This section stays on what the wrapper structurally is and who it fits.

Why accept a tax bill now instead of deferring it? Because a saver who expects to be in a steeper band later can prefer to settle at today's known rate. Augusta does not run that projection for the customer. The dedicated agent explains the wrapper difference, and the rest belongs to the saver's own tax professional.

How Do SEP and SIMPLE Augusta Gold IRAs Work for the Self-Employed?

A SEP-IRA is the employer-funded wrapper built for self-employed savers and small-business owners. A SIMPLE-IRA is the small-employer salary-deferral wrapper. The defining difference from a personal Traditional or Roth account is that eligibility here turns on business status, not just a paycheck.

These two structures are the part of the type map working business owners most often skip. A sole proprietor with a side consultancy, a two-person design studio, a self-employed contractor with freelance income, none of them is limited to a personal wrapper. The SEP and SIMPLE exist precisely because business income needs a structure a personal IRA was never built to carry.

Take the SEP first. It is established by the business, and the funding comes from the employer side. For a sole proprietor or single-member LLC, the owner wears both hats at once, employer and participant, which is what gives the SEP a far larger structural runway than a personal wrapper. The structural signature is the employer-funded design. The dollar ceiling that comes with it is a tax figure, deliberately not quoted here.

The SIMPLE works differently. It pairs an employee salary deferral with an employer contribution, which makes it the structure a small business reaches for when a full corporate plan is too heavy and a SEP does not fit the headcount. A self-employed saver weighing Augusta should treat the SIMPLE as a genuinely separate option from the SEP, not a variant of it. Which one fits depends on whether there are employees and how the owner wants contributions to flow, and the SEP-versus-SIMPLE limit and deduction mechanics are owned in full by the Augusta gold IRA tax benefits guide.

Does Augusta treat a business owner differently at onboarding? No. The same education-first sequence and the same salaried, non-commissioned agent handle a SEP or SIMPLE applicant exactly as they handle a personal one. That parity is itself the point Augusta's founder built the model around.

"He launched Augusta Precious Metals to give retirement savers the education and tools to diversify their savings through precious metals products," noted Augusta Precious Metals on its founder author page.

SEP and SIMPLE eligibility, like every account-type rule behind a self-directed precious-metals IRA, shifts with new legislation, and the structural picture here reflects the publication date. Confirm the current treatment with a tax professional or IRS-approved custodian before establishing a business-funded account.

Can Spouses Open Augusta Precious Metals Accounts Together?

Yes, but the structure is two separate accounts, not one shared one. An IRA is individual by definition, so a married couple holds two distinct Augusta accounts, each with its own custodian record. A spousal arrangement lets a lower-earning or non-earning spouse fund a separate account based on household earned income.

The structural fact comes first. There is no such thing as a joint IRA. The letter I in the abbreviation means individual, full stop. A couple that wants bullion in retirement savings for both partners is therefore looking at two distinct arrangements, each opened and titled separately, not one shared pot.

The spousal mechanism is what makes that work for a single-income household. A non-earning or low-earning partner cannot fund an arrangement on a paycheck they do not have. The structural fix is that the household's earned income, sourced from the working partner, is what permits the second arrangement to be funded at all. The dollar ceiling on that contribution is a tax figure, owned by the tax page, not quoted here.

Separate titling carries a second structural consequence couples often want. Each arrangement names its own beneficiary on its own. One partner can direct a metal arrangement to the children while the other points elsewhere entirely. What happens tax-wise to an inherited arrangement is, again, a mechanic the dedicated tax page owns.

The practical Augusta wrinkle is that the entry minimum noted earlier applies to each arrangement on its own, not to the household as a unit. Two arrangements mean the threshold is cleared twice, which is what shapes the order a couple opens them and how a household splits what it moves. The step-by-step of opening either one sits on the Augusta Precious Metals application process guide. Circumstances differ, so a licensed financial or tax professional should confirm the structure before a couple acts on it.

Which Augusta Account Type Is Right for You?

The right structure depends on three things: whether your funding source is pre-tax or after-tax, your employment status, and your bracket expectation. That is a decision a licensed tax professional should confirm, not one Augusta makes for you. The structural attributes below frame the choice without making it.

Start with the decision tree, not the tax math. The funding source narrows the field fastest. A pre-tax 401(k) or Traditional IRA balance points toward a Traditional wrapper. After-tax money or a higher-future-bracket expectation points toward a Roth. Business income points toward a SEP or SIMPLE. The structure tends to follow the situation rather than the other way around.

The table below compares the structures on their structural attributes only. It does not show contribution dollars, phase-out brackets, or distribution divisors, because those are tax mechanics owned by the dedicated tax page.

| Structure | Funding Source | Broadly Suits | Owner-Lifetime Forced Distribution |

| **Traditional** | Pre-tax rollover or contribution | Lower expected retirement bracket | Yes |

| **Roth** | After-tax dollars or conversion | Higher expected retirement bracket, estate transfer | No |

| **SEP** | Employer (self-employed) | Self-employed and small-business owners | Yes |

| **SIMPLE** | Salary deferral plus employer | Small-business plans | Yes |

One structural point gets missed often. The choice is not strictly one-or-the-other, and it is not permanent. A saver can hold more than one type at once, for example a rollover Traditional account plus a SEP for business income, each a separate Augusta account. The structure is stackable, which is why the single-best type is really a question about your full situation.

Augusta's role here is structural orientation, not advice. The dedicated agent walks the wrapper differences so the customer understands what each container does. Augusta states that its representatives earn salaries rather than per-transaction commissions. The same salaried model is described on Augusta's homepage. That detail matters for trust, because no per-transaction incentive steers a saver toward one wrapper. The bracket projection still comes from the saver's own tax professional. The full bracket math sits on the Augusta gold IRA tax benefits guide.

"Equity Trust is our #1 preferred custodian, but you'll always have full transparency and the freedom to choose the best fit for your gold IRA," explained Augusta Precious Metals on its gold IRA page.

The same posture extends to the structure decision. The choice of type is yours to make with your own professional, not one a salesperson should make for you.

One caution belongs with the type decision specifically. A wrapper choice should follow the saver's tax situation, not a seller's incentive to close the fastest-converting structure. When a representative steers toward a particular type without first asking about the funding source and the bracket outlook, that is a signal worth pausing on. Augusta's published posture runs the other way, with a salaried agent and an education-first sequence. The company has operated since its 2012 founding under Isaac Nuriani, and Money magazine named Augusta Best Overall Gold IRA Company annually from 2022 through 2025 and recognized it for educational resources in 2026. The fuller reputation and ratings picture, including the broader category red flags, is owned by the Augusta Precious Metals review rather than repeated here.

Always consult your own legal, financial, and tax professionals before choosing an account type or opening an Augusta gold IRA.

Frequently Asked Questions

What account types does Augusta Precious Metals offer?

Augusta Precious Metals supports the standard IRS individual retirement arrangements: Traditional, Roth, SEP, and SIMPLE, plus a spousal arrangement for married couples. Each is the same federal wrapper holding IRS-eligible physical gold and silver, differing in tax timing and who can fund it. Augusta is the metals dealer, not the IRA custodian. A separate IRS-approved custodian, with Equity Trust Company as Augusta's number-one preferred, holds whichever account type you choose and files the tax forms.

Can I open a Roth gold IRA with Augusta?

Yes. The Roth structure is available through Augusta, funded with after-tax dollars or by converting a Traditional balance. Structurally it is identical to a Traditional account around the metal, with the tax timing reversed and no required distributions during the original owner's lifetime. The Roth income limits, the five-year rule, and the tax cost of a conversion are tax mechanics covered in full on the Augusta gold IRA tax benefits guide rather than here.

Does Augusta offer SEP IRAs for self-employed savers?

Yes. A SEP-IRA is the employer-funded wrapper built for self-employed savers and small-business owners, and a SIMPLE-IRA is the small-employer salary-deferral wrapper. Both still resolve to a self-directed precious-metals account holding the same IRS-eligible gold and silver through the same custodian and depository chain. Structural eligibility is tied to business status. The contribution dollar limits that separate a SEP from a SIMPLE are tax mechanics routed to the tax benefits page.

Can my spouse and I open separate Augusta accounts?

Yes. An IRA is individual by definition, so a married couple holds two separate Augusta accounts, each with its own custodian record and its own beneficiary. A spousal arrangement lets a working spouse's earned income structurally support a separate account for a non-earning spouse. The $50,000 Augusta minimum applies per account, so each of the two accounts clears its own entry gate, which shapes how a couple sequences the two openings.

Which Augusta account type is best?

There is no single best type. The right structure depends on whether your funding source is pre-tax or after-tax, your employment status, and your expected retirement tax bracket. A pre-tax rollover points toward a Traditional wrapper, after-tax or higher-bracket expectations point toward a Roth, and business income points toward a SEP or SIMPLE. The structures are stackable, so a saver can hold more than one. A licensed tax professional should confirm the choice. Augusta does not choose for you.

Does the $50,000 minimum apply to every account type?

Yes. Augusta Precious Metals requires a $50,000 minimum to open a precious-metals IRA, the highest minimum among major providers, and that gate applies regardless of which IRA structure you choose. The minimum is set by Augusta and could change, so confirm the current figure with the dedicated agent before assuming it still applies. For a married couple opening two separate accounts, the minimum applies to each account individually rather than to the household.

Risk Warning: Precious metals investments carry risk, including the possible loss of principal. Gold and silver prices can fluctuate based on macroeconomic conditions, currency movements, and market sentiment. Past performance is not a guarantee of future results, and historical context is illustrative only. A gold IRA is a long-term diversification tool, not a short-term trading vehicle. IRS rules governing self-directed IRAs and account-type eligibility are complex and change with new legislation. Always consult your own licensed legal, financial, and tax professionals before choosing an account type or opening a gold IRA.

About the Editorial Team

Augusta Precious Metals Reviews is the editorial site covering Augusta Precious Metals. We publish articles about Augusta's products, leadership, fees, customer experience, and gold IRA account structures under an editorial team byline. Our coverage cites named third-party authorities (Internal Revenue Service, Consumer Affairs, Money Magazine) and Augusta's own published positioning. We do not publish urgent, scarcity-driven, or high-pressure content. Editorial review process is documented on the About page.